Macro Outlook

Growth strengthened, but only slightly. In August, industrial output rose 4.2% y/y, up 0.4 pps, lifting overall January-August growth to 3.6%, up 0.1 pps. Investment rose 5.8% y/y in January-August, up 0.1 pps. The August growth rate was 6.4% y/y, up 2.8 pps. Real estate investment growth rate fell further, to -13.8% y/y, down 1.7 pps from August 2021.

In August 2022, consumption rose 5.5% y/y, up 2.7 pps. This is partly due to the low base number of last year, when consumption rose 2.5%, and was down 6 pps from August 2021.

Exports rose 11.8% y/y, down 12.1 pps from July 2022. This seems partially because all major countries except China are exiting from monetary expansion, leading to weakened demand. This month was the first time where exports to the United States had negative growth of -3.8% y/y, dragging down total export growth by 3 pps.

PPI rose 2.3% y/y in August, down 1.9 pps. A major contributing factor is that the production material price growth rate was down 2.6 pps. CPI rose 2.5% y/y, down 0.2 pps from July. Monetary policy remained neutral. At the end of August, M0 rose 14.3% y/y, up 0.4 pps from July. M1 increased 6.1% y/y, down 0.6 pps from July. M2 rose 12.2% y/y, up 0.2 pps.

The offshore exchange rate of the Chinese yuan versus the U.S. dollar recently breached the 7:1 mark for the first time in over two years. Similar to other global currencies that have depreciated in 2022, the yuan’s decline is being driven by the strengthening of the dollar. However, the yuan “basket index” has been relatively stable, and the yuan is unlikely to see significant depreciation, given our forecast of a good balance of payments and overall macroeconomic recovery from further stimulative fiscal policy in the coming months. Other major currency determinants are also sound for the yuan, including a high position for the interest rate and foreign reserves.

Industrial output grew 3.5% y/y in January-July, up 0.1 pps from H1. In January-July, investment rose 5.7% y/y, down 0.4 pps from H1. In particular, the investment growth rate in July was down 2.4 pps from June. High infrastructure investment has been flattened by reduced real estate investment.

Retail sales of social consumption goods fell -0.2% y/y in January-July, up 0.5 pps from January-June. Exports were still strong. In July, exports rose 23.9% y/y, up 1.9 pps from June. Due to the stop of global monetary policy easing, the continuing Ukraine crisis, and the ongoing pandemic, other countries have not recovered well, giving more opportunities to Chinese companies.

PPI and CPI continued to converge. In July, the global crude oil price dropped significantly, leading the overall price level in China to fall. PPI rose 4.2% y/y, down 1.9 pps. CPI rose 2.7% y/y, up 0.2 pps from June, mainly driven by food prices. Monetary policy is easing, but at a small scale due to inflation concern. In the end of July, M0 rose 13.9% y/y, up 0.1 pps from June. M1 rose 6.7% y/y, up 0.9 pps. M2 rose 12% y/y, up 0.6 pps.

The real estate market has been cooling for over a year, and has become particularly cold. In August, China’s property sales plunged almost a third, more than during the 2008 financial crisis. Real estate investment growth fell further to -12.3%, after falling -9.4% in June and -10.1% in April. The real estate sector takes one third of GDP, and so receives much attention. We view the picture as completely different from the 2008 U.S. housing crisis. It is the Chinese government who started this real estate deleveraging, in view of potential future financial problems, and so it is largely manageable. There are also complementary policies, such as bailing out home buyers. Risk is containable, but the process is painful, and will take some time.

GDP only grew 2.5% y/y in H1. As the pandemic shock has been gradually under control and the start of various economic stabilization policies, the recovery growth in June has lifted the Q2 growth to achieve positive growth at 0.4% y/y, contributing to the path “back to normal”.

In H1, industrial output rose 3.4% y/y, down 3.1 pps from Q1. In H1, investment growth rate was 6.1% y/y, down 3.2 pps from Q1, but still 1.2 pps faster than 2021. The continuing real estate cooling does not see any time ending.

Pandemic lockdowns suppressed consumption. Retail sales of social consumption goods fell -0.7% y/y, down 4 pps from Q1. Survey data shows Chinese consumers are pessimistic about future income growth putting more constraint on future consumption recovery. In H1, exports rose 13.2% y/y. In June alone, exports rose 22% y/y, accelerating since April, and is an important force lifting economic recovery.

In H1, PPI rose 7.7% y/y. CPI increased 1.7% y/y. Low inflation benefits from the recovery of supply chains, domestically and internationally. However, future inflation pressure is still high. The main financial indicators were loosened somewhat countercyclically. At the end of June, M2 rose 11.4% y/y, up 0.3 pps from May, and up 1.7 pps from Q1, slowly picking up. M1 rose 5.8% y/y, up 1.2 pps from May, and up 1.1 pps from Q1.

China’s unemployment situation is worsening. According to the National Bureau of Statistics, the government official source, China’s youth unemployment rate for ages from 18 to 24 hit an all-time high of 19.3% in June. It was a sharp rise from 18.4% in May and marked a year-on-year increase of 25%. We believe the unemployment might not pose a society crisis. Parents in China usually provide living net. The unemployment leans more to friction cause. For example, many campus recruitments were suspended because of the pandemic.

Government will continue its effort to bring the economic activities to a higher level. However, it seems not necessary for China to stimulate the economy by additional measures. On July 20th, China’s Prime Minister Li Keqiang stated that China will not adopt large stimulus policies.

Because of the long Chinese New Year holiday, the statistics bureau only announced price, financial and PMI data in February. Producer prices grew more slowly. PPI rose 9.1% y/y, down another 1.2 pps from December. The ex-factory price index of industrial goods rose 8.85% y/y, while CPI growth also slowed. CPI rose 0.9% y/y in January, down 0.6 pps from December. In particular, food prices fell -3.8% y/y, down 2.6 pps from December, dragging CPI down 0.72 pps. That is the leading factor lowering CPI. The falling price levels offer ample room for further money expansion.

At the end of January, M2 rose 9.8% y/y, up 0.8 pps from the end of December, and up 0.4 pps from January 2020. M2 is not strongly affected by the Spring Festival effect. The significant trending upward reflects expansionary monetary policy. M1 fell -1.9% y/y. The adjusted growth rate after taking out the effect of the New Year’s holiday was around 2%. M0 rose 18.5% y/y, a major increase.

The societal financing scale increased by 6.17 trillion yuan in January, much higher than in January 2020, and market expectations. The societal financing scale increased 10.5% y/y, up 0.2 pps from December. The structural composition of societal financing is also improving. PMI fell, but was still in the improvement zone in January. In particular, PMI was 51%, down 1.2 pps from December. This indicates that the overall economic situation is good, and in an expansion zone, but the trend is slowing.

The Ministry of Finance disclosed on February 14th that to that date, some 1.788 trillion yuan ($278 billion) of this year's newly-increased debt limit of local government bonds had been allocated in advance. Of the amount already allocated, 1.46 trillion yuan is for the local government special bond quota. We expect this expansionary fiscal policy to bolster local government financing needs and investment, to ensure growth stability. The early distribution will also have a larger spillover effect for the rest of the year. The government debt ratio in China is still much lower than it in the United States, so financial risk should be containable.

The COVID-19 lockdowns in Shanghai and some other cities since late March have halted the strong economic recovery. In Q1, GDP was up 4.8% y/y, up 0.8 pps from Q4 2021, but 0.2 pps lower than in Q1 2020. Industrial output rose 6.5% in Q1, up

2.6 ppts from Q4, but down 1 pps from January-February. Investment rose 9.3% y/y in Q1, up 4.4 pps from 2021, but 2.9 pps lower than in January-February.

In March, overall PMI, manufacturing PMI, and non-manufacturing business activity PMI were 48.8%, 49.5% and 48.4% respectively, all falling steeply from the previous month, demonstrating that the economic environment has been shrinking in all dimensions.

In Q1, retail sales of consumption goods were up 3.3% y/y, down 9.2, 0.2 and 3.4 pps from 2021, this January and February respectively. In March, consumption fell -3.5% y/y; restaurant income fell -16.4% y/y, its first negative turn after more than one year.

Exports rose 13.4% y/y in Q1, down 4.6 and 0.2 pps from Q4 2021, January-February. Weak export is more because of foreign weakening demand factors, including the Russia-Ukraine war and the Fed raising rates, than because of domestic lockdowns.

In Q1, PPI rose 8.7% y/y, down 3.5 pps from Q4. Production material slowdown is the main reason for lagging PPI growth, and its growth rate was 4.8 pps, down from Q4. In Q1, CPI rose 1.1% y/y, higher than last year. In March, CPI rose 1.5% y/y, a clear rise from January and February. We expect higher CPI to persist.

Shanghai, China’s largest economic and financial center, has been under lockdown since March 27th. On April 26th, Beijing was put on Omicron alert. China's yuan fell to a one-year low, at 6.5 against a strengthening dollar on April 25th, extending losses after posting its worst week since 2015. The economy will be volatile in the near term. However, a depreciating yuan benefits export. The Chinese government is also accelerating fiscal expansion to keep the economy afloat. For example, infrastructure investment rose 8.5% y/y in Q1, up 8.1 and 0.4 pps from last year and January- February respectively.

Executive summary

Because of the long Chinese New Year holiday, the statistics bureau only announced price, financial and PMI data in February. Producer prices grew more slowly. PPI rose 9.1% y/y, down another 1.2 pps from December. The ex-factory price index of industrial goods rose 8.85% y/y, while CPI growth also slowed. CPI rose 0.9% y/y in January, down 0.6 pps from December. In particular, food prices fell -3.8% y/y, down 2.6 pps from December, dragging CPI down 0.72 pps. That is the leading factor lowering CPI. The falling price levels offer ample room for further money expansion.

At the end of January, M2 rose 9.8% y/y, up 0.8 pps from the end of December, and up 0.4 pps from January 2020. M2 is not strongly affected by the Spring Festival effect. The significant trending upward reflects expansionary monetary policy. M1 fell -1.9% y/y. The adjusted growth rate after taking out the effect of the New Year’s holiday was around 2%. M0 rose 18.5% y/y, a major increase.

The societal financing scale increased by 6.17 trillion yuan in January, much higher than in January 2020, and market expectations. The societal financing scale increased 10.5% y/y, up 0.2 pps from December. The structural composition of societal financing is also improving. PMI fell, but was still in the improvement zone in January. In particular, PMI was 51%, down 1.2 pps from December. This indicates that the overall economic situation is good, and in an expansion zone, but the trend is slowing.

The Ministry of Finance disclosed on February 14th that to that date, some 1.788 trillion yuan ($278 billion) of this year's newly-increased debt limit of local government bonds had been allocated in advance. Of the amount already allocated, 1.46 trillion yuan is for the local government special bond quota. We expect this expansionary fiscal policy to bolster local government financing needs and investment, to ensure growth stability. The early distribution will also have a larger spillover effect for the rest of the year. The government debt ratio in China is still much lower than it in the United States, so financial risk should be containable.

Producer prices rose more slowly

Because of the long Chinese New Year holiday, in January (as usual), the statistics bureau only announced price, PMI index and financial data. So the analysis does not cover much. In January, PMI fell, but was still in an improvement zone. The detailed classification indicates that demand is still weak, but also suggests that market expectations are improving.

Faster money growth and societal financing scale indicate that the real economy’s financing demand has recovered. We expect fiscal policy to be intensive as well, with infrastructure projects accelerating their pace of construction. The lowering overall price level also lends a possibility for further monetary loosening. With the Spring Festival effect, part of the non-food and service categories’ price supports further CPI appreciation. But pork prices are falling significantly. The two opposite changes keep the CPI stable.

From the published data, in January, PPI rose 9.1% y/y, further down 1.2 pps from December. In particular, production material price rose 11.8% y/y, down 1.6 pps from December. Living material prices rose 0.8% y/y, down 0.2 pps.

The production material price fluctuation is the main factor driving the ex-factory price index of industrial goods. The latter rose around 8.85% y/y. Its slowdown is the main factor pushing down PPI growth.

For specific industries, main industries that saw their prices growing more slowly are coal, oil and gas, black metal mining and refinery. Those industries rose 51.3%, 38.2%, 30.1%, and 14.7% y/y, down 15.5, 7.4, 6.3, and 6.7 pps respectively.

GRAPH 1

Change in CPI and Ex-Factory Price Index of Industrial Products (y/y, %)

Source: Chinese State Statistical Bureau

Source: Chinese State Statistical Bureau

Purchasing prices of industrial producers rose 12.1% y/y, and fell -0.4% m/m. The latter’s growth rate is down more from December than the y/y growth rate, leading the ex-factory price index to fall.

The main price compositions of gas, chemical, and black metal related materials rose 30%, 17.9%, and 9.8% y/y, and fell -0.9%, -1.1%, and -0.7% m/m respectively, driving PPI had its m/m growth rate negative.

The slowdown of the ex-factory price index and PPI show that central government policies to beat down prices have been effective. The slowdown of PPI m/m growth rate led to coal mining, and black metal refinery to decrease -3.5% and -1.9% m/m, contributing to the overall industrial good price to fall. But affected by global oil and gas price increase, domestic oil and gas mining price rose 2.6%, up 9.5 pps from December. The globally dependent nature of oil and gas leads to their large fluctuations from the global factor.

CPI growth also slows

CPI rose 0.9% y/y in January, down 0.6 pps from December. In particular, food prices fell -3.8% y/y, down 2.6 pps from December, dragging down CPI around 0.72 pps. That is the leading factor lowering CPI.

Pork prices fell -41.6% y/y, because of the high base number of last year, down 4.9 pps from December, which instead is the main factor leading the food price decline. Vegetable price fell -4.1% y/y, down 14.7 pps from December. For m/m growth rates, food price rose 1.4% m/m, up 2 pps from December. The Spring Festival effect has pushed up fruit and seafood price to increase 7.2% and 4.1% m/m respectively, which are the main factor keeping up the food price.

Non-food prices rose 2% y/y, down only 0.1 pps from December. The high demand for oil and gas from the transportation demand increase due to the New Year’s holiday effect is the main contributing factor to non-food price increase. Specifically, gasoline and diesel oil prices rose 20.7% and 22.7% y/y respectively, which then contribute to industrial good price to rise 2.5% y/y.

The service price index rose 1.7% y/y, up 0.2 pps from December. This was mostly due to airfare and household related service prices rising 20.8% and 6.2% y/y.

For m/m growth rates, prices for oil, diesel oil, and gas rose 2.2%, 2.4%, and 1.5% m/m. Air tickets, transportation rental fees and long-distance coach prices rose 12.4%, 9.8%, and 5.2% m/m. House cleaning, babysitting and haircut prices rose between 2.6% and 9.1% m/m. After we take out the food and energy factors as compositions of CPI, the other prices rose 1.2% y/y overall, the same rate as in December, indicating the overall CPI growth is mild.

Signs of expansionary monetary policy

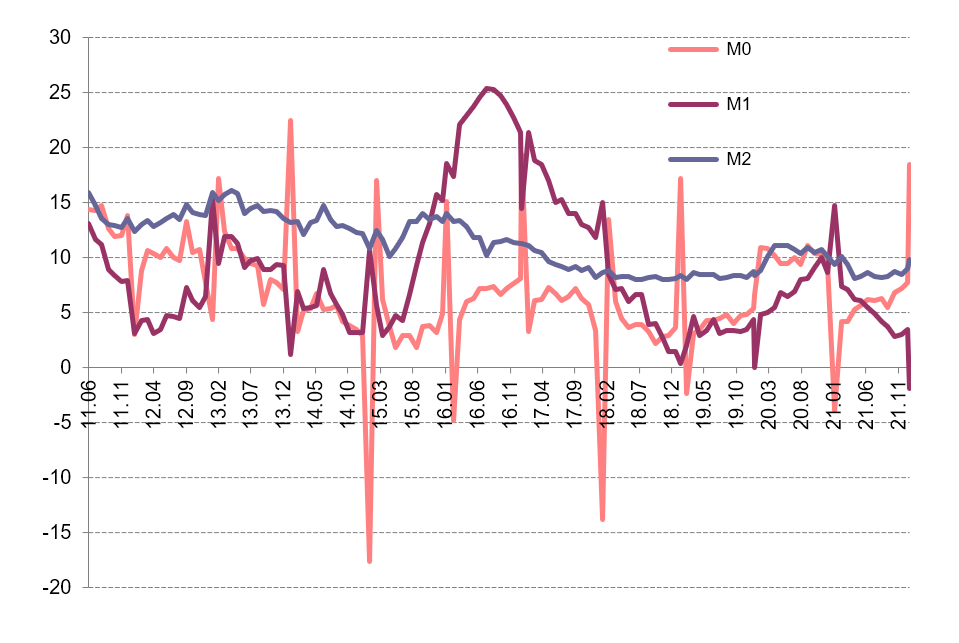

M2 was up 9.8% y/y at the end of January, up 0.8 pps from the end of December, and up 0.4 pps from January 2020. M2 is not strongly affected by the Spring Festival effect. The significant trending upward reflects expansionary monetary policy.

M1 fell -1.9% y/y. The adjusted growth rate after taking out the Spring Festival effect was around 2%. M0 rose 18.5% y/y, a large increase. What the changes of M0 and M1 reflect are the Spring Festival effect. It is customary for firms to distribute compensation and welfare in a lump-sum way to households. This leads to the transition from enterprise saving to individual savings. As seen from the data, household savings increased 5.41 trillion yuan, and non-financial enterprises savings reduced 1.4 trillion yuan. But M1 growth rate is lower than expectation probably because house purchase intention is still low in January. It is hard for household saving to transit to enterprise savings.

GRAPH 2

Change in M0, M1, and M2 (y/y, %)

Source: Chinese State Statistical Bureau

The societal financing scale increased by 6.17 trillion yuan in January, much higher than in January 2020, and market expectations. The societal financing scale increased 10.5% y/y, up 0.2 pps from December.

The structural composition of societal financing is also improving. In particular, RMB loans under the customary societal financing standard increased 4.2 trillion yuan, 380.6 billion yuan more than last January. Government bond net financing rose 579.9 billion yuan, 188.2 billion more than last January. The aggregate of trusted loan, entrusted loan, and non-discounted bank note increased 447.9 billion yuan, 32.8 billion yuan more than last January.

Loans, corporate debt, and bank outside-balance-sheet business had major increases, except regulatory delay for government bond financing and private company to go public.

Our analysis above shows that the societal financing scale increased significantly; its composition structure also improved. Both of these show that, with all the efforts from back-to-normal monetary policy, less regulation for commercial banks, and infrastructure acceleration, monetary policy has more and more impacts on the real economy.

PMI fell, but remained in an improvement zone

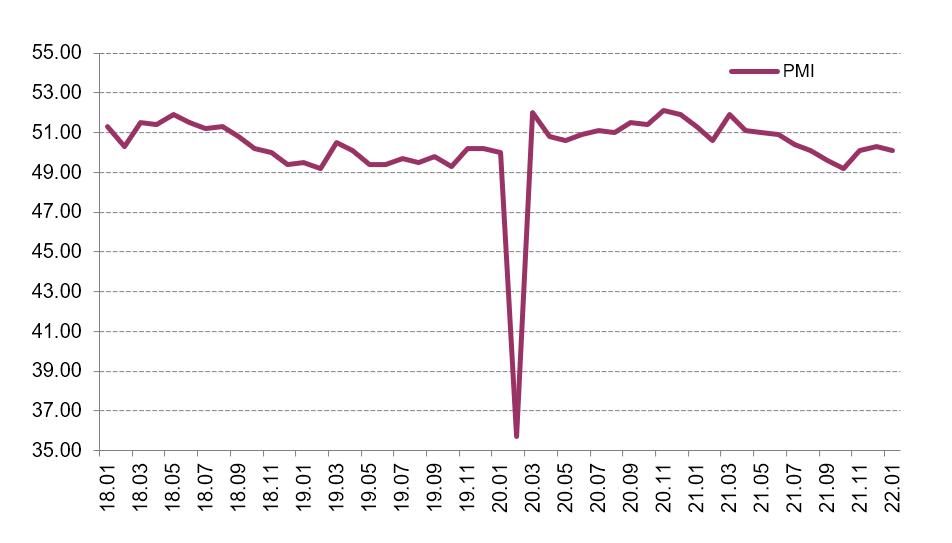

Overall PMI was 51% in January, down 1.2 pps from December. This indicates that the general economic situation is good, and in an expansionary zone, but the trend is falling.

In particular, manufacturing PMI was 50.1%, down 0.2 pps from December. This is also consistent with the overall economy, which is still in an expansionary zone, but with slowing growth.

GRAPH 3

PMI Index (y/y, %)

Source: CEIC data

Non-manufacturing PMI was 51.1%, down 1.6 pps from December. This is also consistent with the overall economic PMI.

For specific categories, new manufacturing orders decreased -0.4% m/m, showing weak demand. But manufacturing activity expectations, new construction orders and related activity rose 3.2, 3.3, and 0.6 m/m from December, and reached their PMI of 57.5%, 53.3%, and 57.9%, reflecting improving market expectations.

Local bond issue acceleration will keep economy stable

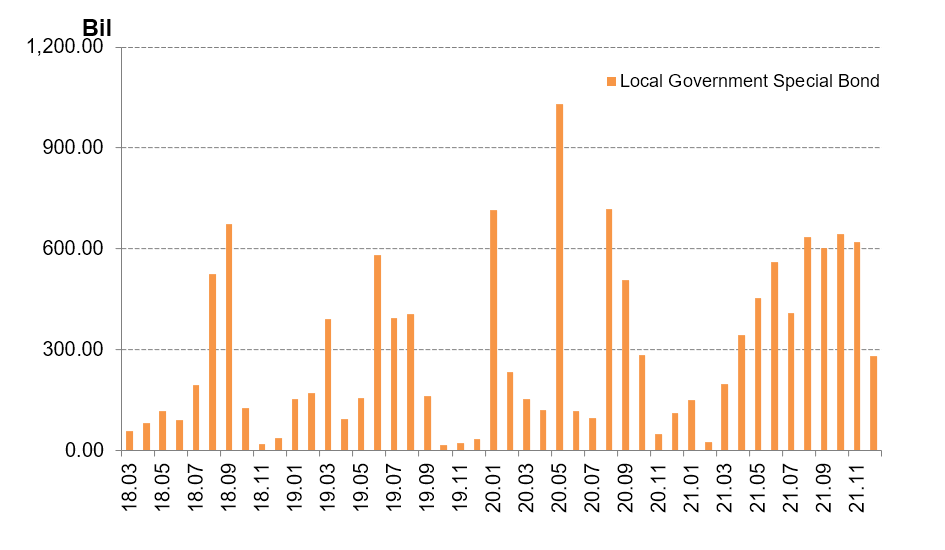

The Ministry of Finance disclosed on February 14th that to date, some 1.788 trillion yuan ($278 billion) of this year's newly increased debt limit of local government bonds had been allocated in advance. Of the amount already allocated, 1.46 trillion yuan is for local government’s special bond quota. We expect this expansionary fiscal policy to help local government’s financing needs and investment, to ensure growth stability. The early distribution will also have a larger spillover effect for the rest of the year. Government debt in China is still much lower than it in the United States, so financial risk should be containable.

Around the same time, on February 22nd, net onshore bond issuance by state-owned enterprises (SOEs) owned by the Henan provincial government turned positive in Q4 2021. Funding conditions stabilized after the default of Yongcheng Coal in November 2020 dampened investor appetite for securities issued by Henan SOEs in H1 2021, then reflected a return of investor confidence.

GRAPH 4

Local Government Special Bond (Billion yuan)

Source: National Bureau of Statistics

Although where local government special bonds will be put into use is not specifically clear, we can draw a big picture from where the bond was allocated last year, and we expect it to still be largely consistent with those fractions, as there is no specific different shock.

In 2021, half of the bond was in the area of transportation infrastructure. From the rough mention for the plan in 2022, the largest category is still transportation infrastructure. Other categories are energy, agriculture --particularly forestry and water -- environmental protection, social security and production chain infrastructure.

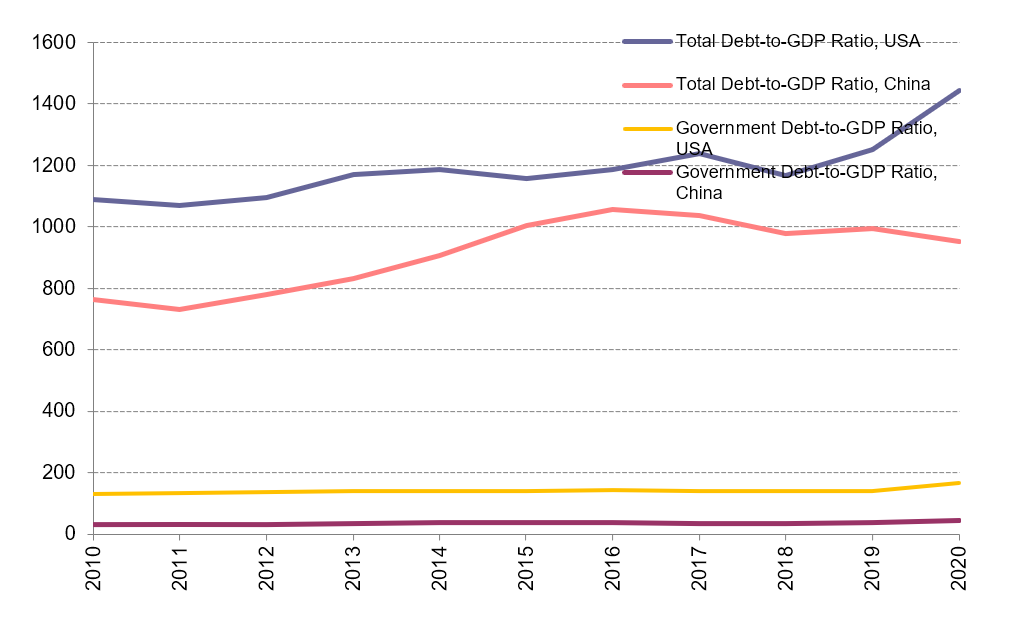

One concern of using these debt-driven infrastructure growth is the whole debt level and potential financial risks. The Chinese government seems to pay particular attention to this issue. All the reports have repeatedly mentioned that the financial risks need to be carefully watched. The graph below also shows that China’s debt ratios are still below those of the United States, leaving further room to add more debt. Compared to other instruments, issuing bonds can contain an inflation and asset bubble.

GRAPH 5

Debt to GDP (%)

Source: National Bureau of Statistics

In our view this special bond has two different advantages over previous local government debt. If the central government simply approves any local government’s request to issue more debt, then there will be strong debt- and capital-misallocation. This is because the poorer regions will have a greater need to issue debt. However, one reason they are poor is due to their low productivity. If money is allocated to such regions, then the expected return should be lower. There will be a vicious cycle under this scenario. The financial market itself might have limited power to discipline because of its state-owned nature. Instead, currently, the central government carefully monitors the approval of these bonds, so that their efficient level should be higher.

Second, the previous local government is mainly financed by local banks. Given crony relations in small local areas, the financing is less efficient compared to the current arrangement. The national financial market that follows greater market discipline will determine bond quantity and pricing.

Growth continues to be weak. In November, industrial output grew 3.8% y/y, down 1.1 pps from Q3, much lower than the growth rates of recent years. Investment is also low, and was up 7.9% y/y, and down 1.2 pps from January-June. Its adjusted growth rate is instead negative. The real estate market is still cold: sales were down -14.2% y/y in November.

Consumption rose 3.9% y/y in November, down 1 pps from October, and its adjusted growth rate was 0.5% y/y, hitting its lowest level this year. But trade is still strong. Imports were up 26% y/y, and up 9.8 pps from Q3. Exports were up16.6% y/y.

Producer price growth finally reversed to a downward trend. The price level of the index of ex-factory industrial goods was the same as in October, and up 12.9% y/y, down 0.6 pps from October. PPI increased 1% m/m, 17.4% y/y from October, up 0.3 pps from October. We expect PPI growth to be slower next month. In November, CPI rose 2.3% y/y, up 0.8 pps from October. Its adjusted growth rate is the same as in October.

Principal financial indicators operated at low levels in November. M2 rose 8.5% y/y, comparable with 2018 and 2019. M1 rose 3%, up only 0.2 pps from the lowest growth rate this year. There is still uncertainty over whether money growth’s downward trend will be reversed. Loan growth has been at its lowest since 1990, for three consecutive months.

The yuan has risen 2.6% against the dollar this year, even with the dollar strengthening 8% since May. This is in contrast to an unexpectedly weaker Chinese economy, and to real estate risks highlighted in the news headlines. Appreciation is likely due to strong export and investor confidence. We expect that the yuan may appreciate mildly in 2022, and that it won’t fall below 6 against the dollar. This is based on an expected stronger dollar, and expectations of further growth slowdown in China in 2022.

Growth has weakened, especially in services. In August, industrial output grew 5.3% y/y, and was up 11.2% from August 2019, with an annualized growth rate of 5.4%, down 0.2 ppts from July, and down 1.2 ppts from Q2. The service production index has slowed since Q2, and grew only 4.8% y/y in August, after being further hit by the COVID outbreaks, down 2.9 ppts from Q4 2020, and down 2.1 ppts from 2019.

Investment was up 8.9% y/y January-August, and increased 8% from August 2019, with an annualized growth rate of 4%, down 0.5 ppt from H1. Real estate is cooling dramatically, to the 2008 financial crisis level. COVID outbreaks in August negatively impacted consumption. Retail sales of social consumption goods rose 2.5% y/y, down 6 ppts from July. Their growth rate after price adjustment was 0.9% y/y. As we forecast, trade became weaker. Exports rose 15.7% y/y, down 4.4 ppts from Q2. Imports rose 23.1% y/y, down 8.5 ppts from Q2.

Producer prices increased further in August. The ex-factory price index of industrial goods rose 9.5% y/y; PPI increased 13.6% y/y, both 0.5 ppts higher from July. However, we forecast that producer price appreciation will stabilize in November, and that prices will begin to fall. CPI rose 0.8% y/y, falling for three consecutive months. We expect the lowering of CPI to be temporary, and to reach around 2%, after food prices stop declining.

In August, monetary policy continued its tightening trend. M2 rose 8.2% y/y, basically stable since April. M1 rose 4.2% y/y, continuing to fall, reaching its the lowest of 2021, down 0.7 ppts from July.

China is announcing intensive policies in specific key areas, to address structural reform. In the financial industry area, President Xi Jinping announced on September 2nd that a third stock exchange in Beijing would be established, in addition to the existing two exchanges in Shanghai and Shenzhen, to serve small and medium-sized businesses. In regional policies, Shenzhen’s Qianhai and Zhuhai’s Hengqin areas are being pushed to deepen their ties with bordering Hong Kong and Macau. The Qianhai economic zone is to expand eightfold. There are also other new industry rules for the real estate and education sectors. All of these plans underscore the central government’s effort to develop a healthier economy, by being more open and more market-based. But policy uncertainty looms over investment in the short term. The possible default of real estate companies such as Evergrande also raises some fear of turmoil in China’s financial market. But we do not see this as a systematic threat.

The Chinese economy has been stably rising in Q2. GDP was up 7.9% y/y, and up 11.4% from Q2 2019, with an annualized growth rate of 5.5%, up 0.5 pps from Q1. Industrial output was up 8.9% y/y, and up 13.7% from Q2 2019, with an annualized growth rate of 6.6% y/y, slightly lower than in Q1 but higher than the pre-pandemic 2019 level; specifically, growth in June was 6.5%.

Investment was up 12.6% y/y, and increased 9.1% from Q2 2019, with an annualized growth rate of 4.4% y/y, up 1.8 pps from Q1, and down 1 pps from 2019. In Q2, retail sales of social consumption goods were up 9.5% from Q2 2019, with an annualized growth rate of 4.6% y/y, up 0.5 pps from Q1. In June, trade continued its strong growth. Exports rose 20.2% y/y, comparable to the average growth rate in March-May, while imports rose 24.4% y/y, up 5 pps from Q1.

Producer price growth slowed in June, but we expect it to pick up soon. The ex-factory price index of industrial goods increased 8.8% y/y, down 0.2 pps from May. CPI rose 1.1% y/y, down 0.2 pps from May, contributed by falling meat prices.

The main financial indicators saw diverging trends in June. The societal financing scale switched from large drops in previous months to positive growth of 7.7% y/y. M1 continues its declining growth trend. At the end of June, M2 rose 8.6% y/y, lower than most of the previous months. M1 rose 5.5% y/y, down 0.6 pps from May.

The pandemic shows no sign of vanishing from the world. This situation makes central banks around the world unlikely to exit from lowered interest rates and other stimulus measures. The vaccine situation in developed countries is much better than in the rest of the world. China’s strong recovery over the past 12 months is mainly derived from exports. This driving growth factor may be weakened by the economic recovery in developed countries, as they resume their production and reduce their demand for China’s exports later this year. China is therefore facing downturn pressures, amid an environment of globally increasing inflation.

Growth was stable in May. Industrial output rose 8.8% y/y, and increased 13.6% from May 2019, with an annualized growth rate of 6.6%. Investment rose 15.4% y/y, and increased 8.5% from May 2019, with an annualized growth rate of 4.2% y/y -- still in a low growth zone.

Consumption has recovered further. In May, retail sales of social consumption goods rose 9.3% y/y from May 2019, with an annualized growth rate of 4.5%, up 0.2 pps from April. Trade has been strong since the beginning of this year, especially for imports, which are growing robustly. In May, imports rose 39.5% y/y. Exports rose 18.1% y/y, down 4.1 pps from April, but still 7.1 pps higher than in Q4 2020.

Producer prices have been appreciating since Q2 2020, and are rising particularly fast this year, most likely from overseas monetary liquidity loosening. In May, the ex-factory price index of industrial output rose 9% y/y. The PPI growth rate reached 12.5% y/y. The growth rates of both were higher than their peak points in 2017 and 2010. In May, CPI rose 1.3% y/y. Although this growth rate is not high, the trend is forming, and picking up.

Monetary and financial indicators kept weakening in May. M2 rose 8.3% y/y. M1 rose 6.1% y/y, down 0.1 pps from April. Saving deposits from non-financial enterprises rose 3.8% y/y, down 1.5 pps from April, reaching their lowest growth rate since 2016.

China’s yuan has strengthened to a near three-year high, reaching 6.4 per dollar on June 21st, boosted by a falling dollar. It has also been buoyed in recent months by the country’s rapid recovery from the pandemic, and by a rush of international investment into China’s relatively high-yielding markets. Chinese stocks also jumped, thanks partly to a surge in foreign buying. A strengthening yuan will bring the current strong exports back to normal. The yuan might still appreciate further with China’s relatively tight monetary policy, in contrast to global monetary loosening, such as the almost zero interest rate in the United States. China’s tightening monetary policy is hardly likely to change, in the face of future global inflation spillover risk.

More...

Growth is stable. Industrial output was up 9.8% y/y in April, and up 14.1% y/y from April 2019, with annualized growth of 6.8% y/y, the same as in Q1, and higher than the pre-pandemic levels in 2018 and 2019. Investment is still weak, and rose 8% y/y from April 2019, with an annualized growth rate of 3.9% y/y, up 1.3 pps from Q1. We expect economic growth to be strong, though fiscal and monetary policy are not loosening. Our forecast is based on strong trade growth from global economic recovery, commodity price appreciation and demand recovery.

Consumption recovered slowly. In April, price-adjusted consumption grew 5.4% y/y from April 2019, with an annualized growth rate of 2.7% y/y. Trade in April continues to be strong. Exports rose 22.2% y/y, up 11 pps from Q4 2020. Imports rose 32.2% y/y, up more than 20 pps from Q4.

Producer prices continue to grow faster. In April, the ex-factory price index of industrial output rose 6.8% y/y, and PPI increased 9% y/y, approaching the peak point in Q1 2017. CPI rose 0.9% y/y, up 0.5 pps from March. Most financial and monetary indicators grew more slowly. At the end of April, M2 rose 8.1% y/y, down 2 pps from the end of 2020. M1 rose 6.2% y/y, down 2.4 pps.

China’s once-in-a-decade population census, with preliminary results announced on May 12th, showed the slowest population growth rate since the 1950s, notwithstanding the relaxation of the one-child policy to a two-child policy in 2016. The census also showed that more Chinese people were moving away from the poorer northeastern part of the country, and to the wealthier eastern and southern regions. For example, Shenzhen and Guangzhou, already among the largest cities previously, gained the most, of 7.13 million and 5.98 million people. The migration to richer and more productive cities, made possible by the relaxation of Hukou, provides a key growth source, simply because labor can be utilized more efficiently.

GDP was up 18.3% y/y in Q1, and up 10.3% from Q1 2019, with an annualized growth rate of around 5%. In this report, we mostly use Q1 2019 as the benchmark period, because the major shock from the pandemic in February 2020 makes Q1 2020 data hardly comparable. The adjusted growth rate was lower than in Q4 2020, and higher than in Q3 2020, and can be viewed as stable.

In Q1 2021, industrial output was up 14% y/y from Q1 2019, with annualized growth of 6.8%, slightly lower than in Q4 2020. In particular, industrial growth in March reached 12.8% y/y, with an annualized growth rate of 6.2% y/y, up 0.4 pps from Q3 2020. In Q1, investment rose 25.6% y/y, and increased only 5.4% from Q1 2019, with an annualized growth rate of 2.6%, much lower than in H2 2020.

In Q1, retail sales of social consumption goods rose 33.9% y/y, and were up 8.5% from Q1 2019, with an annualized growth rate of 4.1%, indicating that consumption is still on its way to recovery. In Q1, imports rallied, and grew 19.2% y/y, up 19.3 pps from Q4 2020. Exports increased 16.5% from Q1 2019. The adjusted growth rate is comparable to H2 2020, and is at high levels for recent years.

In Q1, producer prices continue to increase, and the growth rates are high. In March, the ex-factory price index and PPI saw growth reach 4.4% and 5.2% y/y, up 4.8 pps and 5.2 pps from December 2020. This is mainly driven by strong demand for commodities from other countries’ economic recoveries. CPI is instead basically stable. Money and financial indicators grew more slowly. At the end of March, M2 was up 9.4% y/y, down 1.5 pps from its peak last year. M1 was up 7.1% y/y, and has decreased 2.9 pps over four consecutive months.

Postponing the retirement age will be on the Chinese government’s agenda, according to announcement made March 22nd, with further details released on April 13th. China’s aging problem is severe, and population growth is on a steep declining trend, and has attracted great attention. The takeaway from the statement on postponing retirement age is that the delay is to be gradual, and experimental. It will alleviate the negative effects of slower population growth. Population aging and slower growth mainly negatively affect GDP, but not necessarily in per capita terms, due to China’s high savings rate, and financially rich central government.

Economic recovery is still going strong. In January-February, industrial output was up 35.1% y/y, and up 16.9% compared to January-February 2019. Annualized growth was 8.1% y/y, higher than all quarterly growth since 2015, and up 1 pps from Q4 2020. Since the Chinese economy was shut down to a large extent last February due to COVID-19, we also look at growth rates for most indicators by comparing their performance with the same period in 2019.

In January-February, investment fell -35% y/y, and was up only 3.5% y/y from the same period in 2019. The investment slowdown is mostly due to the central government’s intention to cool the economy.

Trade is strong, as we forecast. In January-February, exports were up 50.1% y/y, and increased by 26.2% from same period in 2019, and up 9 pps from Q4 2020. Imports were up 14.5% y/y. The adjusted growth rate was around 12% y/y, up 12.1 pps from Q4.

Producer prices rose faster. In February, the ex-factory price index of industrial goods was up 1.7% y/y, and up 1.4 pps from January. The PPI was up 2.4% y/y, and up 1.5 pps from January. The CPI fell -0.2% y/y, up 0.1 pps from January. Monetary policy has returned to normal. At the end of February, M2 was up 10.1% y/y, the same rate as the end of last year, and down 1 pps from the peak last year. M1 rose 7.4%, down 2.6 pps from the peak last year, and it has declined rapidly since November.

Consumption is the only weak indicator. In January-February, retail sales of social consumption goods were up 33.8% y/y, up 6.4% from same period in 2019, and up 1.8 pps from Q4 2020, indicating consumption demand is still on a path of recovery.

On March 23rd, Premier Li Keqiang said that China’s economic growth this year could exceed a target of “above 6%,” with the government seeking stable expansion and job creation, emphasizing consumption. Consumption inequality, which is closely related to income and wealth equality, rose last year. With the premier’s effort and return to normal monetary policy, we believe consumption as well as the much-related imports will rise this year.

Producer prices increased fast between June 2020 and January 2021, and finally turned positive. The ex-factory price index of industrial goods rose 1% m/m, and 0.3% y/y. PPI rose 1.4% m/m, and 0.9% y/y. We expect the ex-factory price index to soon rise higher than 5% y/y, and PPI will rise higher than 8% y/y.

CPI fell -0.3% y/y. However, its seasonally adjusted growth rate was 0.3% m/m. The rise of the CPI level is mainly driven by the strong rebound of meat prices. The rebound is temporary, and linked to the Spring Festival effect. We expect the meat price will continuously drop for the next few months, and for CPI growth to slow as well.

Monetary and financial indicators cooled further. In January, M2 rose 9.4% y/y, down 0.7 pps from December. M1 rose 14.7% y/y, and 10% y/y after taking out the Spring Festival effect. RMB loans from financial institutions rose 12.7% y/y, down 0.1 pps from December. Savings deposits from non-financial institutions rose 15.8% y/y and deposits’ adjusted growth rate was lower than 12% y/y. Because the broad money supply was not affected by the Spring Festival effect, their growth rate declines show that the overall money and financial situation continue their declining trend.

PMI fell. In January 2021, PMI was 51.3%, down 0.6 pps from December 2020. The non-manufacturing business activity index was 52.4% y/y, down 3.3 pps from December. The two indexes show that expansion trends for both manufacturing and non-manufacturing industries have slowed.

Chinese exports have been strong since 2020. For example, China overtookthe United States as Europe’s top trade partner in 2020. Even though pandemic-related goods comprise a sizable share, other categories’ exports are also rising. Strong export growth, with production interruption in the rest of the world because of the pandemic, shows China’s economic resilience. The resumption of overseas production, if the pandemic is under control, will lift Chinese exports of capital and intermediate goods. Moreover, the import demand from the United States had been strong since 2020, and will likely be large, given the incoming stimulus. In sum, robust export performance will persist, and we expect export growth in the first half of 2021 to be 16%.

")

")

")

")

")

")

")

")